Demystifying Investing: Your Comprehensive Guide to Basic Investing Terms

Affiliate disclosure: This article may contain affiliate links. Recommendations are independent and editorially driven.

Embarking on your investment journey can feel like learning a new language. The world of finance is rich with specific jargon, and understanding these basic investing terms is the first crucial step towards making informed decisions and building lasting wealth. At assetbar, we believe that financial literacy is the cornerstone of successful investing for everyone, especially retail investors.

This comprehensive guide is designed to cut through the complexity, providing clear, concise explanations of the fundamental concepts, instruments, market mechanics, and strategies you’ll encounter. Whether you’re just starting with micro-investing or looking to deepen your understanding of asset allocation, mastering these terms will empower you to navigate the financial markets with confidence and clarity. Let’s break down the essential vocabulary together, transforming what might seem daunting into understandable, actionable knowledge.

The Foundation: Core Concepts of Investing

Before diving into specific assets or complex strategies, it’s vital to grasp the foundational principles that underpin all investment activities. These basic investing terms are the bedrock upon which all successful financial planning is built.

Investment vs. Savings

While often used interchangeably by newcomers, “investment” and “savings” serve distinct purposes in personal finance. Savings typically refers to money set aside for short-term goals or emergencies, usually held in highly liquid accounts like savings accounts or money market accounts, where the primary objective is capital preservation and easy access. While these accounts offer security, they often yield minimal returns, sometimes not even keeping pace with inflation.

An investment, conversely, is money allocated with the expectation of generating a future return or appreciating in value over time. The goal is wealth accumulation, usually for medium to long-term objectives like retirement, buying a home, or funding education. Investments involve a degree of risk – the possibility of losing some or all of your principal – but also offer the potential for significantly higher returns than traditional savings, allowing your money to work harder for you.

Compounding: The “Eighth Wonder of the World”

Albert Einstein is famously quoted as calling compound interest the “eighth wonder of the world,” and for good reason. Compounding is the process where the earnings from your initial investment are reinvested, generating their own earnings. This creates a snowball effect, as your money grows exponentially over time. Instead of just earning returns on your original principal, you start earning returns on your principal plus all the accumulated interest and gains from previous periods.

For example, if you invest $1,000 and earn 5% interest, you get $50. In the next period, you earn 5% on $1,050, then on $1,102.50, and so on. The longer your money is invested, the more powerful compounding becomes. This is why starting early, even with small amounts, is a cornerstone of effective wealth building.

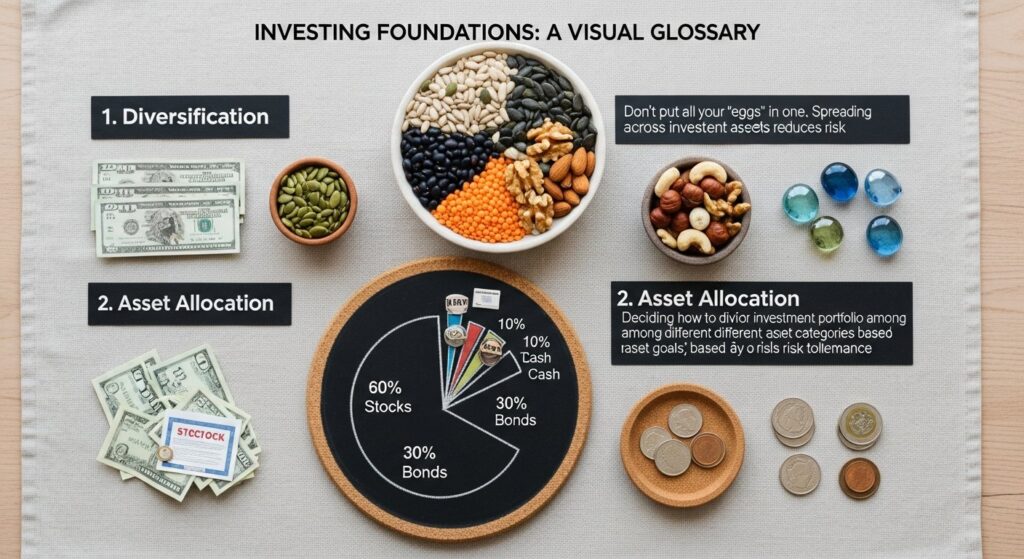

Diversification: Spreading Your Bets

One of the most crucial basic investing terms, diversification is a risk management strategy that involves mixing a wide variety of investments within a portfolio. The rationale is to minimize the impact of any single security or asset class performing poorly. By spreading your investments across different types of assets (e.g., stocks, bonds, real estate), industries, geographies, and company sizes, you reduce your overall exposure to risk.

The saying “don’t put all your eggs in one basket” perfectly encapsulates diversification. If one part of your portfolio experiences a downturn, other parts might be performing well, thus smoothing out your overall returns and protecting your capital. Diversification is key to robust asset allocation strategies.

Risk and Return: The Inseparable Pair

In finance, risk and return are intrinsically linked. Generally, higher potential returns are associated with higher levels of risk. This relationship is a fundamental concept in investing. Return refers to the profit or loss generated on an investment over a period, typically expressed as a percentage of the initial investment. Risk is the possibility that the actual return will differ from the expected return, including the potential loss of some or all of the original investment.

Understanding your personal risk tolerance – how much financial loss you are comfortable enduring – is critical for selecting appropriate investments. Low-risk investments (like government bonds) typically offer lower returns, while high-risk investments (like growth stocks or emerging market funds) have the potential for greater gains but also greater losses.

Liquidity: How Quickly Can You Get Your Cash?

Liquidity refers to the ease with which an investment can be converted into cash without significantly affecting its market price. A highly liquid asset can be sold quickly at its fair market value, such as a stock of a large publicly traded company. Cash itself is the most liquid asset.

Illiquid assets, like real estate or private equity investments, can take time to sell and convert into cash, and their sale price might be more susceptible to market conditions or the urgency of the seller. Understanding the liquidity of your investments is important for financial planning, especially when considering short-term financial needs.

Understanding Investment Vehicles: Where to Put Your Money

Once you grasp the foundational concepts, the next step is to understand the various avenues available for investment. These basic investing terms describe the different types of assets you can add to your portfolio.

Stocks (Equities): Owning a Piece of a Company

When you buy stocks, also known as equities, you are purchasing a small ownership stake in a company. As a shareholder, you have a claim on the company’s assets and earnings proportional to the number of shares you own. Stocks are considered growth investments, as their value can appreciate significantly if the company performs well. They also offer the potential for income through dividends, which are distributions of a company’s profits to its shareholders.

- Common Stock: Represents ownership in a company and a claim (dividends) on a portion of profits. Investors get voting rights in corporate decisions.

- Preferred Stock: Generally carries no voting rights, but has a higher claim on assets and earnings than common stock. Preferred stock usually pays fixed dividends.

- Blue-Chip Stocks: Stocks of large, well-established, and financially sound companies with a long history of reliable earnings and dividends.

- Growth Stocks: Stocks of companies expected to grow at an above-average rate compared to other companies in the market. They often reinvest earnings back into the business rather than paying dividends.

- Value Stocks: Stocks that trade at a price lower than their intrinsic value, often identified by fundamental analysis. Investors believe the market has undervalued them.

Bonds (Fixed Income): Lending Money for Interest

A bond is essentially a loan made by an investor to a borrower (typically a corporation or government). When you buy a bond, you are lending money to the issuer, who agrees to pay you back the original amount (the principal or face value) on a specific date (the maturity date) and to pay you periodic interest payments (the coupon rate) along the way. Bonds are considered fixed-income investments because they typically provide a predictable stream of income.

- Coupon Rate: The annual interest rate paid on a bond, expressed as a percentage of the face value.

- Maturity Date: The date on which the principal amount of a bond is repaid to the investor.

- Yield: The return an investor receives on a bond. There are various types, like current yield and yield to maturity (YTM), which consider the bond’s price relative to its face value and coupon rate.

- Corporate Bonds: Issued by companies to raise capital.

- Government Bonds: Issued by national governments (e.g., U.S. Treasury bonds) or local governments (municipal bonds). Generally considered lower risk.

Mutual Funds: Professionally Managed Portfolios

A mutual fund is a type of investment vehicle consisting of a portfolio of stocks, bonds, or other securities. It is operated by a professional money manager who invests pooled money from multiple investors. Mutual funds offer diversification, professional management, and liquidity. Investors buy shares in the fund, and the value of these shares (Net Asset Value or NAV) fluctuates based on the performance of the underlying assets.

- Net Asset Value (NAV): The price per share of a mutual fund, calculated by dividing the total value of the fund’s assets (minus liabilities) by the number of outstanding shares.

- Load Funds: Mutual funds that charge a sales commission (load) either at the time of purchase (front-end load) or sale (back-end load).

- No-Load Funds: Mutual funds that do not charge a sales commission.

- Actively Managed Fund: A fund where a manager makes specific investment decisions with the goal of outperforming a benchmark index.

- Index Fund: A type of mutual fund designed to track the performance of a specific market index (e.g., S&P 500). They are typically passively managed and have lower fees.

Exchange-Traded Funds (ETFs): Like Mutual Funds, but Traded Like Stocks

An Exchange-Traded Fund (ETF) is a type of investment fund that holds assets such as stocks, commodities, or bonds, and trades on stock exchanges like regular stocks. Unlike mutual funds, which are priced once per day after the market closes, ETFs can be bought and sold throughout the trading day at their market price. ETFs typically offer diversification and lower expense ratios than actively managed mutual funds, as many are designed to track an index.

The growing popularity of ETFs among retail investors for their flexibility and cost-efficiency makes them one of the most important basic investing terms to understand. Many micro-investing platforms utilize ETFs to provide diversified portfolios with low entry barriers. Learn more about the benefits of ETFs for beginners.

Real Estate (REITs): Investing in Property Without Buying a House

Directly owning physical real estate can be a significant investment, but you can gain exposure to the real estate market through Real Estate Investment Trusts (REITs). A REIT is a company that owns, operates, or finances income-producing real estate. They are often publicly traded, allowing individual investors to buy shares in portfolios of large-scale properties such as apartment complexes, shopping malls, offices, and hotels. REITs offer diversification and typically pay high dividends, but they are also subject to market and interest rate risks.

- Equity REITs: Own and operate income-producing real estate.

- Mortgage REITs (mREITs): Provide financing for income-producing real estate by purchasing or originating mortgages and mortgage-backed securities.

Commodities: Raw Materials as Investments

Commodities are basic goods used in commerce that are interchangeable with other goods of the same type. These raw materials, like oil, gold, silver, natural gas, agricultural products (corn, wheat), and industrial metals, can be bought and sold. Investors typically gain exposure to commodities through futures contracts, options, or commodity ETFs/mutual funds, rather than directly owning the physical goods. Commodities can act as a hedge against inflation and offer diversification, as their prices often move independently of stock and bond markets.

Market Mechanics and Players: How the Market Works

Understanding where and how investments are bought and sold, and the roles of different participants, is crucial for any aspiring investor. These basic investing terms explain the infrastructure and key players of the financial world.

Stock Market, Bond Market: The Arenas of Trade

The stock market is a collective term for the exchanges and other venues where stocks are bought and sold. Its primary function is to facilitate the issuance and exchange of equity securities. Major stock exchanges include the New York Stock Exchange (NYSE) and NASDAQ. The stock market provides a platform for companies to raise capital and for investors to trade ownership stakes.

The bond market, also known as the debt market or credit market, is where participants can issue new debt, known as the primary market, or buy and sell debt securities, known as the secondary market. It is larger than the stock market and encompasses a vast array of debt instruments issued by governments, corporations, and municipalities.

Brokerage Accounts: Your Gateway to Investing

A brokerage account is a financial account that allows you to buy and sell investment assets like stocks, bonds, mutual funds, and ETFs. These accounts are typically offered by brokerage firms (like assetbar), which act as intermediaries between investors and the financial markets. There are different types of brokerage accounts:

- Full-Service Brokerage: Offers a wide range of services, including personalized advice, financial planning, and research, but typically comes with higher fees.

- Discount Brokerage: Provides lower-cost access to trading platforms and research tools, with less or no personalized advice. Ideal for self-directed investors.

- Robo-Advisor: An automated digital platform that provides algorithm-driven financial planning services with little to no human supervision, often with very low fees. assetbar offers robo-advisory features for optimized asset allocation.

Market Order vs. Limit Order: How to Place Your Trades

When you want to buy or sell a security, you place an order with your broker. Understanding the difference between a market order and a limit order is essential:

- A market order is an order to buy or sell a security immediately at the best available current price. It prioritizes execution speed over price, meaning your order will almost certainly be filled, but the exact price might fluctuate slightly, especially in volatile markets.

- A limit order is an order to buy or sell a security at a specific price or better. A buy limit order will only execute at the limit price or lower, while a sell limit order will only execute at the limit price or higher. Limit orders guarantee price, but there’s no guarantee the order will be filled if the market price never reaches your specified limit.

Bid-Ask Spread: The Cost of Trading

The bid-ask spread is the difference between the highest price a buyer is willing to pay for an asset (the “bid” price) and the lowest price a seller is willing to accept (the “ask” price). This spread represents the market’s liquidity and is how market makers and brokers profit from facilitating trades. A narrow spread indicates high liquidity and efficient pricing, while a wide spread suggests less liquidity and potentially higher trading costs for investors. Understanding this is key to optimizing your entry and exit points in the market.

Bull Market vs. Bear Market: Market Sentiment

These terms describe the overall trend and sentiment in the financial markets:

- A bull market is characterized by rising stock prices, investor optimism, and economic growth. It reflects a period where investors are confident and expect prices to continue to rise.

- A bear market, conversely, is characterized by falling stock prices, investor pessimism, and economic contraction. It’s a period where investors anticipate prices to decline further.

Both are part of the natural cycle of markets, and understanding these trends helps investors contextualize short-term fluctuations within long-term strategies.

Key Performance & Valuation Metrics: Measuring Success

To assess the health and potential of an investment, you need to understand how to measure its performance and value. These basic investing terms are critical for fundamental analysis and portfolio evaluation.

Return on Investment (ROI): The Bottom Line

Return on Investment (ROI) is a fundamental metric used to evaluate the profitability of an investment. It measures the gain or loss generated on an investment relative to its initial cost. ROI is typically expressed as a percentage and is calculated as: (Current Value of Investment - Cost of Investment) / Cost of Investment. A positive ROI indicates a profit, while a negative ROI indicates a loss. It’s a simple, widely used metric for comparing the efficiency of different investments.

Annualized Return: Standardizing Performance

While ROI gives a snapshot, annualized return adjusts the return of an investment over a specific period (longer than one year) to a yearly average. This allows for a fair comparison between investments held for different durations. For instance, an investment that returned 20% over two years isn’t as good as one that returned 20% over one year. Annualizing standardizes these returns, making them comparable on a per-year basis and providing a clearer picture of long-term growth.

Dividends: Income from Ownership

Dividends are a portion of a company’s profits paid out to its shareholders. Not all companies pay dividends; growth companies often reinvest profits back into the business, while more mature companies might distribute dividends regularly. Dividends can be a significant source of income for investors, particularly those in retirement, and contribute to the total return of an investment. They are typically paid quarterly and can be reinvested to buy more shares, amplifying the power of compounding.

- Dividend Yield: The annual dividend per share divided by the stock’s current share price, expressed as a percentage. It indicates the return on investment from dividends alone.

Earnings Per Share (EPS): A Company’s Profitability Measure

Earnings Per Share (EPS) is a key financial metric that indicates how much net profit a company makes for each outstanding share of common stock. It’s calculated by dividing a company’s net income (minus preferred dividends) by the number of outstanding common shares. A higher EPS generally indicates a more profitable company, and it is a widely watched indicator for assessing a company’s financial health and potential for growth. Investors often look at EPS trends over time.

Price-to-Earnings (P/E) Ratio: Valuation at a Glance

The Price-to-Earnings (P/E) ratio is one of the most popular valuation metrics for stocks. It measures a company’s current share price relative to its per-share earnings. Calculated as: Market Value Per Share / Earnings Per Share. The P/E ratio indicates how much investors are willing to pay for each dollar of a company’s earnings. A high P/E ratio might suggest that investors expect high future growth, while a low P/E ratio could indicate an undervalued stock or a company with slower growth prospects. It’s best used when comparing companies within the same industry.

Market Capitalization: Company Size

Market capitalization (Market Cap) is the total value of a company’s outstanding shares. It’s calculated by multiplying the company’s current stock price by the total number of its outstanding shares. Market cap is used to categorize companies into different sizes:

- Large-Cap: Typically companies with a market cap of $10 billion or more. These are often established, stable companies.

- Mid-Cap: Companies with a market cap between $2 billion and $10 billion. They often represent growth potential beyond large-caps but with more stability than small-caps.

- Small-Cap: Companies with a market cap between $300 million and $2 billion. These are often younger companies with high growth potential but also higher risk.

Market cap is an important factor in asset allocation and understanding the risk/reward profile of different segments of the stock market.

Risk Management and Strategy: Navigating Uncertainty

Investing inherently involves risk, but smart investors employ strategies to manage and mitigate it. These basic investing terms are fundamental to building a resilient portfolio and achieving long-term goals.

Volatility: The Degree of Price Fluctuation

Volatility refers to the degree of variation of a trading price series over time. In simpler terms, it measures how much an investment’s price fluctuates. A highly volatile asset experiences rapid and significant price swings, while a low-volatility asset has more stable prices. While high volatility can present opportunities for quick gains, it also carries a greater risk of significant losses. Understanding an investment’s volatility helps investors assess its risk profile and potential impact on their portfolio.

Asset Allocation: Spreading Across Asset Classes

Asset allocation is the strategic process of dividing an investment portfolio among different asset categories, such as stocks, bonds, and cash equivalents. The goal is to balance risk and reward by adjusting the percentage of each asset in relation to an investor’s goals, time horizon, and risk tolerance. For instance, younger investors with a longer time horizon might opt for a higher percentage of stocks (more aggressive), while those nearing retirement might prefer a higher percentage of bonds (more conservative). This is a cornerstone of effective portfolio management, and platforms like assetbar often assist users with optimized asset allocation.

Dollar-Cost Averaging: Smoothing Out Market Swings

Dollar-cost averaging (DCA) is an investment strategy in which an investor invests a fixed amount of money at regular intervals (e.g., $100 every month) into a particular asset, regardless of its price. This strategy helps to reduce the impact of volatility because you buy more shares when prices are low and fewer shares when prices are high, ultimately leading to a lower average cost per share over time. DCA is particularly effective for long-term investors and is a common practice in micro-investing and regular contributions to retirement accounts. Discover how dollar-cost averaging can benefit your investment strategy.

Portfolio Rebalancing: Staying on Track

Portfolio rebalancing is the process of adjusting the weightings of assets in a portfolio back to their original target allocations. Over time, the performance of different assets can cause a portfolio’s allocation to drift from its intended targets. For example, if stocks perform exceptionally well, they might grow to represent a larger percentage of your portfolio than initially desired. Rebalancing involves selling some of the outperforming assets and buying more of the underperforming assets to restore the desired proportions. This systematic approach helps maintain the intended risk level and ensures your portfolio remains aligned with your financial goals.

Risk Tolerance: Your Comfort Zone with Loss

Risk tolerance refers to an individual’s willingness and ability to take on financial risk. It’s a critical factor in determining an appropriate investment strategy. Investors with a high risk tolerance might be comfortable with more volatile investments in pursuit of higher returns, understanding that they might experience significant losses. Those with a low risk tolerance prefer safer, less volatile investments, even if it means lower potential returns. Understanding your own risk tolerance is fundamental to building a portfolio that allows you to sleep soundly at night, regardless of market fluctuations.

Understanding Costs and Fees: The Hidden Impact on Returns

Every investment comes with associated costs. While some are obvious, others can be subtle but significantly impact your long-term returns. Being aware of these basic investing terms related to fees is essential for maximizing your net gains.

Expense Ratios: The Cost of Fund Management

For mutual funds and ETFs, the expense ratio is a crucial fee to understand. It’s an annual fee charged as a percentage of your investment to cover the fund’s operating expenses, including management fees, administrative costs, and marketing expenses. For example, an expense ratio of 0.50% means you pay $5 annually for every $1,000 invested. Even small differences in expense ratios can add up to substantial amounts over decades due to the power of compounding. Passively managed index funds and many ETFs typically have much lower expense ratios than actively managed funds.

Commission Fees: Trading Costs

A commission fee is a charge levied by a broker or financial institution for executing a trade (buying or selling securities). Historically, commissions were a significant cost for investors, but with the rise of discount brokers and robo-advisors (like assetbar), many platforms now offer commission-free trading for stocks and ETFs. However, commissions can still apply to certain types of trades, options, or mutual funds, so it’s important to check the fee schedule of your brokerage.

Management Fees: For Professional Oversight

Management fees are charges paid to investment managers or financial advisors for overseeing and managing your investment portfolio. These fees can be part of a fund’s expense ratio or a separate charge for personalized advisory services. They are typically calculated as a percentage of the assets under management (AUM). While professional management can be valuable, it’s crucial to understand the fee structure and ensure the value provided justifies the cost, especially for asset allocation services.

Advisory Fees: For Personalized Guidance

Separate from fund management fees, advisory fees are paid to financial advisors for personalized financial planning, investment advice, and portfolio management services. These fees can be structured in several ways: a percentage of AUM, an hourly rate, a flat fee, or a combination. When working with a financial advisor, understanding their fee structure and how it aligns with your financial goals is paramount. Robo-advisors often offer a lower-cost alternative for basic advisory services.

Investment Accounts and Tax Implications: Navigating the Tax Landscape

The type of account you use to hold your investments can have significant tax implications, affecting your net returns. Understanding these basic investing terms related to accounts and taxes is vital for tax-efficient investing.

Taxable Brokerage Accounts: Flexible but Taxed

A taxable brokerage account is a standard investment account where earnings and capital gains are subject to taxes in the year they are realized. There are no contribution limits, and you can withdraw funds at any time. While offering maximum flexibility, these accounts do not provide the tax advantages of retirement accounts. Interest income, dividends, and capital gains (when you sell an investment for a profit) are typically taxable. Understanding the difference between short-term and long-term capital gains is important here.

Retirement Accounts (401(k), IRA): Tax-Advantaged Growth

Retirement accounts are specially designed investment vehicles that offer significant tax benefits to encourage saving for retirement. The two most common types for retail investors are 401(k)s and Individual Retirement Accounts (IRAs).

- 401(k): An employer-sponsored retirement plan that allows employees to contribute a portion of their salary before taxes are withheld. Contributions and earnings grow tax-deferred until retirement. Many employers also offer a matching contribution, which is essentially “free money.”

- Individual Retirement Account (IRA): A personal retirement savings plan.

- Traditional IRA: Contributions are often tax-deductible in the year they are made, and earnings grow tax-deferred. You pay taxes on withdrawals in retirement.

- Roth IRA: Contributions are made with after-tax dollars, meaning they are not tax-deductible. However, qualified withdrawals in retirement are entirely tax-free.

The choice between a Traditional and Roth account often depends on your current income level and expected tax bracket in retirement. These accounts are cornerstones of long-term wealth building due to their powerful tax advantages. Explore different retirement account options for your future.

Capital Gains: Profits from Selling Investments

Capital gains are the profits realized when you sell an investment for more than its purchase price (its “cost basis”). These gains are subject to taxation. The tax rate applied depends on how long you held the investment:

- Short-Term Capital Gains: Gains from assets held for one year or less are typically taxed at your ordinary income tax rate, which can be higher.

- Long-Term Capital Gains: Gains from assets held for more than one year are taxed at preferential, lower rates. This encourages long-term investing.

Understanding the distinction is crucial for tax planning and can influence your holding periods for various investments.

Tax-Loss Harvesting: Reducing Your Taxable Income

Tax-loss harvesting is a strategy investors use to reduce their tax liability by selling investments at a loss to offset capital gains and, in some cases, a limited amount of ordinary income. For example, if you realize $5,000 in capital gains from one investment, you can sell another investment that has lost $5,000 to offset those gains, effectively reducing your taxable gains to zero. You can also use up to $3,000 of net capital losses to offset ordinary income each year, carrying forward any excess losses to future years. This strategy needs careful planning to avoid wash-sale rules.

The Role of Financial Professionals and Resources: Getting Help and Staying Informed

You don’t have to navigate the investment world alone. Various professionals and resources are available to assist you. Understanding these basic investing terms will help you choose the right support for your financial journey.

Financial Advisors: Personalized Guidance

A financial advisor is a professional who helps individuals and organizations manage their money. They can provide a wide range of services, including investment advice, retirement planning, estate planning, and insurance analysis. Advisors can be fee-only (paid directly by clients), commission-based (paid by selling products), or fee-based (a combination). When choosing an advisor, it’s important to look for a fiduciary, meaning they are legally obligated to act in your best interest.

Robo-Advisors: Automated, Low-Cost Advice

A robo-advisor is a digital platform that provides automated, algorithm-driven financial planning services with little to no human supervision. These platforms typically offer automated portfolio management, rebalancing, and tax-loss harvesting based on your risk tolerance and financial goals, often at a much lower cost than traditional human advisors. assetbar’s micro-investing platform utilizes robo-advisory features to simplify asset allocation and make sophisticated investing accessible to retail investors, even with small amounts of money.

Financial News and Research: Staying Informed

Staying updated with financial news and research is crucial for making informed investment decisions. This includes reading reputable financial publications, analyzing company reports (like annual reports and quarterly earnings statements), following economic indicators, and understanding market trends. While it’s important not to react to every piece of news, being informed helps you understand the broader economic landscape and the factors influencing your investments.

Micro-Investing Platforms (like assetbar): Investing Made Accessible

Micro-investing platforms (like assetbar) are financial services that allow individuals to invest very small amounts of money, often by rounding up everyday purchases or setting up recurring small contributions. These platforms break down the traditional barriers to entry for investing, making it accessible to a broader audience, including those with limited capital. They often simplify the investment process, provide diversified portfolios, and encourage consistent investing through dollar-cost averaging, making them an excellent starting point for new investors.

Investment Vehicle Comparison Table

To help illustrate the differences among common investment vehicles, here’s a comparative overview:

| Investment Vehicle | Primary Goal | Typical Risk Level | Income Potential | Liquidity | Key Benefit for Retail Investors |

|---|---|---|---|---|---|

| Stocks (Equities) | Capital Appreciation | Medium to High | Dividends, Capital Gains | High | High growth potential; direct ownership in companies. |

| Bonds (Fixed Income) | Income Generation, Capital Preservation | Low to Medium | Interest Payments (Coupon) | Medium to High | Stability, predictable income, portfolio diversification. |

| Mutual Funds | Diversification, Professional Management | Varies (Fund Specific) | Dividends, Interest, Capital Gains | High (daily NAV pricing) | Instant diversification, managed by experts. |

| Exchange-Traded Funds (ETFs) | Diversification, Index Tracking | Varies (Fund Specific) | Dividends, Capital Gains | High (trades like stocks) | Low cost, diversification, trading flexibility. |

| Real Estate (REITs) | Income Generation, Long-term Growth | Medium | High Dividends | Medium (traded on exchanges) | Exposure to real estate without direct property ownership; high dividends. |

Conclusion: Your Path to Financial Empowerment

Mastering these basic investing terms is more than just memorizing definitions; it’s about building a foundational understanding that empowers you to take control of your financial future. From the fundamental difference between saving and investing to the nuances of asset allocation and tax-efficient strategies, each term unlocks a new level of insight into how markets work and how you can participate effectively.

At assetbar, our mission is to make financial literacy and successful investing accessible to everyone. By demystifying the jargon and providing clear explanations, we aim to equip retail investors like you with the knowledge and tools needed to make smart, confident investment decisions. Remember, investing is a journey of continuous learning. Start small, stay consistent, diversify your portfolio, and always seek to expand your understanding. With a solid grasp of these basic investing terms, you are well on your way to achieving your wealth-building goals and securing a prosperous future.

Frequently Asked Questions

Q1: What are the absolute must-know basic investing terms for a beginner?

A1: For a beginner, the most crucial basic investing terms to understand include “investment,” “savings,” “compounding,” “diversification,” “risk and return,” “stocks,” “bonds,” “ETFs,” and “mutual funds.” Grasping these foundational concepts will provide a solid framework for making your first investment decisions and understanding broader market dynamics.

Q2: How do I know if I have a high or low risk tolerance?

A2: Your risk tolerance is your willingness and ability to endure potential losses for higher gains. You can assess it by considering your financial goals (time horizon), current financial situation (emergency fund, debt), and emotional reaction to market fluctuations. If the thought of losing a significant portion of your capital keeps you up at night, you likely have a lower risk tolerance. Many brokerage platforms, including assetbar, offer questionnaires to help you determine your risk tolerance more accurately.

Q3: What’s the main difference between a mutual fund and an ETF?

A3: Both mutual funds and ETFs pool money from investors to buy a diversified portfolio of securities. The main difference lies in how they are traded and priced. Mutual funds are priced once a day after the market closes (based on their Net Asset Value or NAV) and are bought/sold directly from the fund company. ETFs, on the other hand, trade like individual stocks on exchanges throughout the day, allowing for real-time buying and selling at fluctuating market prices. ETFs often have lower expense ratios and more trading flexibility.

Q4: Why is diversification so important, and how can I achieve it with basic investing terms?

A4: Diversification is crucial because it helps reduce risk by spreading your investments across various assets, industries, and geographies. If one investment performs poorly, others may perform well, cushioning the impact on your overall portfolio. You can achieve diversification by investing in a mix of stocks and bonds, using broad-market ETFs or mutual funds that hold hundreds or thousands of different securities, and considering different asset classes like real estate (via REITs) or commodities.

Q5: Are all investment accounts taxable?

A5: Not all investment accounts are fully taxable in the same way. While standard brokerage accounts (taxable accounts) generate taxable events from interest, dividends, and capital gains in the year they occur, retirement accounts like 401(k)s and IRAs (Traditional and Roth) offer significant tax advantages. Traditional accounts allow tax-deferred growth (you pay taxes upon withdrawal in retirement), while Roth accounts offer tax-free withdrawals in retirement (after-tax contributions). Understanding these differences is key to optimizing your tax strategy.

Demystifying Investing: Your Comprehensive Guide to Basic Investing Terms

Affiliate disclosure: This article may contain affiliate links. Recommendations are independent and editorially driven.

Embarking on your investment journey can feel like learning a new language. The world of finance is rich with specific jargon, and understanding these basic investing terms is the first crucial step towards making informed decisions and building lasting wealth. At assetbar, we believe that financial literacy is the cornerstone of successful investing for everyone, especially retail investors.

This comprehensive guide is designed to cut through the complexity, providing clear, concise explanations of the fundamental concepts, instruments, market mechanics, and strategies you’ll encounter. Whether you’re just starting with micro-investing or looking to deepen your understanding of asset allocation, mastering these terms will empower you to navigate the financial markets with confidence and clarity. Let’s break down the essential vocabulary together, transforming what might seem daunting into understandable, actionable knowledge.

The Foundation: Core Concepts of Investing

Before diving into specific assets or complex strategies, it’s vital to grasp the foundational principles that underpin all investment activities. These basic investing terms are the bedrock upon which all successful financial planning is built.

Investment vs. Savings

While often used interchangeably by newcomers, “investment” and “savings” serve distinct purposes in personal finance. Savings typically refers to money set aside for short-term goals or emergencies, usually held in highly liquid accounts like savings accounts or money market accounts, where the primary objective is capital preservation and easy access. While these accounts offer security, they often yield minimal returns, sometimes not even keeping pace with inflation.

An investment, conversely, is money allocated with the expectation of generating a future return or appreciating in value over time. The goal is wealth accumulation, usually for medium to long-term objectives like retirement, buying a home, or funding education. Investments involve a degree of risk – the possibility of losing some or all of your principal – but also offer the potential for significantly higher returns than traditional savings, allowing your money to work harder for you.

Compounding: The “Eighth Wonder of the World”

Albert Einstein is famously quoted as calling compound interest the “eighth wonder of the world,” and for good reason. Compounding is the process where the earnings from your initial investment are reinvested, generating their own earnings. This creates a snowball effect, as your money grows exponentially over time. Instead of just earning returns on your original principal, you start earning returns on your principal plus all the accumulated interest and gains from previous periods.

For example, if you invest $1,000 and earn 5% interest, you get $50. In the next period, you earn 5% on $1,050, then on $1,102.50, and so on. The longer your money is invested, the more powerful compounding becomes. This is why starting early, even with small amounts, is a cornerstone of effective wealth building.

Diversification: Spreading Your Bets

One of the most crucial basic investing terms, diversification is a risk management strategy that involves mixing a wide variety of investments within a portfolio. The rationale is to minimize the impact of any single security or asset class performing poorly. By spreading your investments across different types of assets (e.g., stocks, bonds, real estate), industries, geographies, and company sizes, you reduce your overall exposure to risk.

The saying “don’t put all your eggs in one basket” perfectly encapsulates diversification. If one part of your portfolio experiences a downturn, other parts might be performing well, thus smoothing out your overall returns and protecting your capital. Diversification is key to robust asset allocation strategies.

Risk and Return: The Inseparable Pair

In finance, risk and return are intrinsically linked. Generally, higher potential returns are associated with higher levels of risk. This relationship is a fundamental concept in investing. Return refers to the profit or loss generated on an investment over a period, typically expressed as a percentage of the initial investment. Risk is the possibility that the actual return will differ from the expected return, including the potential loss of some or all of the original investment.

Understanding your personal risk tolerance – how much financial loss you are comfortable enduring – is critical for selecting appropriate investments. Low-risk investments (like government bonds) typically offer lower returns, while high-risk investments (like growth stocks or emerging market funds) have the potential for greater gains but also greater losses.

Liquidity: How Quickly Can You Get Your Cash?

Liquidity refers to the ease with which an investment can be converted into cash without significantly affecting its market price. A highly liquid asset can be sold quickly at its fair market value, such as a stock of a large publicly traded company. Cash itself is the most liquid asset.

Illiquid assets, like real estate or private equity investments, can take time to sell and convert into cash, and their sale price might be more susceptible to market conditions or the urgency of the seller. Understanding the liquidity of your investments is important for financial planning, especially when considering short-term financial needs.

Understanding Investment Vehicles: Where to Put Your Money

Once you grasp the foundational concepts, the next step is to understand the various avenues available for investment. These basic investing terms describe the different types of assets you can add to your portfolio.

Stocks (Equities): Owning a Piece of a Company

When you buy stocks, also known as equities, you are purchasing a small ownership stake in a company. As a shareholder, you have a claim on the company’s assets and earnings proportional to the number of shares you own. Stocks are considered growth investments, as their value can appreciate significantly if the company performs well. They also offer the potential for income through dividends, which are distributions of a company’s profits to its shareholders.

- Common Stock: Represents ownership in a company and a claim (dividends) on a portion of profits. Investors get voting rights in corporate decisions.

- Preferred Stock: Generally carries no voting rights, but has a higher claim on assets and earnings than common stock. Preferred stock usually pays fixed dividends.

- Blue-Chip Stocks: Stocks of large, well-established, and financially sound companies with a long history of reliable earnings and dividends.

- Growth Stocks: Stocks of companies expected to grow at an above-average rate compared to other companies in the market. They often reinvest earnings back into the business rather than paying dividends.

- Value Stocks: Stocks that trade at a price lower than their intrinsic value, often identified by fundamental analysis. Investors believe the market has undervalued them.

Bonds (Fixed Income): Lending Money for Interest

A bond is essentially a loan made by an investor to a borrower (typically a corporation or government). When you buy a bond, you are lending money to the issuer, who agrees to pay you back the original amount (the principal or face value) on a specific date (the maturity date) and to pay you periodic interest payments (the coupon rate) along the way. Bonds are considered fixed-income investments because they typically provide a predictable stream of income.

- Coupon Rate: The annual interest rate paid on a bond, expressed as a percentage of the face value.

- Maturity Date: The date on which the principal amount of a bond is repaid to the investor.

- Yield: The return an investor receives on a bond. There are various types, like current yield and yield to maturity (YTM), which consider the bond’s price relative to its face value and coupon rate.

- Corporate Bonds: Issued by companies to raise capital.

- Government Bonds: Issued by national governments (e.g., U.S. Treasury bonds) or local governments (municipal bonds). Generally considered lower risk.

Mutual Funds: Professionally Managed Portfolios

A mutual fund is a type of investment vehicle consisting of a portfolio of stocks, bonds, or other securities. It is operated by a professional money manager who invests pooled money from multiple investors. Mutual funds offer diversification, professional management, and liquidity. Investors buy shares in the fund, and the value of these shares (Net Asset Value or NAV) fluctuates based on the performance of the underlying assets.

- Net Asset Value (NAV): The price per share of a mutual fund, calculated by dividing the total value of the fund’s assets (minus liabilities) by the number of outstanding shares.

- Load Funds: Mutual funds that charge a sales commission (load) either at the time of purchase (front-end load) or sale (back-end load).

- No-Load Funds: Mutual funds that do not charge a sales commission.

- Actively Managed Fund: A fund where a manager makes specific investment decisions with the goal of outperforming a benchmark index.

- Index Fund: A type of mutual fund designed to track the performance of a specific market index (e.g., S&P 500). They are typically passively managed and have lower fees.

Exchange-Traded Funds (ETFs): Like Mutual Funds, but Traded Like Stocks

An Exchange-Traded Fund (ETF) is a type of investment fund that holds assets such as stocks, commodities, or bonds, and trades on stock exchanges like regular stocks. Unlike mutual funds, which are priced once per day after the market closes, ETFs can be bought and sold throughout the trading day at their market price. ETFs typically offer diversification and lower expense ratios than actively managed mutual funds, as many are designed to track an index.

The growing popularity of ETFs among retail investors for their flexibility and cost-efficiency makes them one of the most important basic investing terms to understand. Many micro-investing platforms utilize ETFs to provide diversified portfolios with low entry barriers. Learn more about the benefits of ETFs for beginners.

Real Estate (REITs): Investing in Property Without Buying a House

Directly owning physical real estate can be a significant investment, but you can gain exposure to the real estate market through Real Estate Investment Trusts (REITs). A REIT is a company that owns, operates, or finances income-producing real estate. They are often publicly traded, allowing individual investors to buy shares in portfolios of large-scale properties such as apartment complexes, shopping malls, offices, and hotels. REITs offer diversification and typically pay high dividends, but they are also subject to market and interest rate risks.

- Equity REITs: Own and operate income-producing real estate.

- Mortgage REITs (mREITs): Provide financing for income-producing real estate by purchasing or originating mortgages and mortgage-backed securities.

Commodities: Raw Materials as Investments

Commodities are basic goods used in commerce that are interchangeable with other goods of the same type. These raw materials, like oil, gold, silver, natural gas, agricultural products (corn, wheat), and industrial metals, can be bought and sold. Investors typically gain exposure to commodities through futures contracts, options, or commodity ETFs/mutual funds, rather than directly owning the physical goods. Commodities can act as a hedge against inflation and offer diversification, as their prices often move independently of stock and bond markets.

Market Mechanics and Players: How the Market Works

Understanding where and how investments are bought and sold, and the roles of different participants, is crucial for any aspiring investor. These basic investing terms explain the infrastructure and key players of the financial world.

Stock Market, Bond Market: The Arenas of Trade

The stock market is a collective term for the exchanges and other venues where stocks are bought and sold. Its primary function is to facilitate the issuance and exchange of equity securities. Major stock exchanges include the New York Stock Exchange (NYSE) and NASDAQ. The stock market provides a platform for companies to raise capital and for investors to trade ownership stakes.

The bond market, also known as the debt market or credit market, is where participants can issue new debt, known as the primary market, or buy and sell debt securities, known as the secondary market. It is larger than the stock market and encompasses a vast array of debt instruments issued by governments, corporations, and municipalities.

Brokerage Accounts: Your Gateway to Investing

A brokerage account is a financial account that allows you to buy and sell investment assets like stocks, bonds, mutual funds, and ETFs. These accounts are typically offered by brokerage firms (like assetbar), which act as intermediaries between investors and the financial markets. There are different types of brokerage accounts:

- Full-Service Brokerage: Offers a wide range of services, including personalized advice, financial planning, and research, but typically comes with higher fees.

- Discount Brokerage: Provides lower-cost access to trading platforms and research tools, with less or no personalized advice. Ideal for self-directed investors.

- Robo-Advisor: An automated digital platform that provides algorithm-driven financial planning services with little to no human supervision, often with very low fees. assetbar offers robo-advisory features for optimized asset allocation.

Market Order vs. Limit Order: How to Place Your Trades

When you want to buy or sell a security, you place an order with your broker. Understanding the difference between a market order and a limit order is essential:

- A market order is an order to buy or sell a security immediately at the best available current price. It prioritizes execution speed over price, meaning your order will almost certainly be filled, but the exact price might fluctuate slightly, especially in volatile markets.

- A limit order is an order to buy or sell a security at a specific price or better. A buy limit order will only execute at the limit price or lower, while a sell limit order will only execute at the limit price or higher. Limit orders guarantee price, but there’s no guarantee the order will be filled if the market price never reaches your specified limit.

Bid-Ask Spread: The Cost of Trading

The bid-ask spread is the difference between the highest price a buyer is willing to pay for an asset (the “bid” price) and the lowest price a seller is willing to accept (the “ask” price). This spread represents the market’s liquidity and is how market makers and brokers profit from facilitating trades. A narrow spread indicates high liquidity and efficient pricing, while a wide spread suggests less liquidity and potentially higher trading costs for investors. Understanding this is key to optimizing your entry and exit points in the market.

Bull Market vs. Bear Market: Market Sentiment

These terms describe the overall trend and sentiment in the financial markets:

- A bull market is characterized by rising stock prices, investor optimism, and economic growth. It reflects a period where investors are confident and expect prices to continue to rise.

- A bear market, conversely, is characterized by falling stock prices, investor pessimism, and economic contraction. It’s a period where investors anticipate prices to decline further.

Both are part of the natural cycle of markets, and understanding these trends helps investors contextualize short-term fluctuations within long-term strategies.

Key Performance & Valuation Metrics: Measuring Success

To assess the health and potential of an investment, you need to understand how to measure its performance and value. These basic investing terms are critical for fundamental analysis and portfolio evaluation.

Return on Investment (ROI): The Bottom Line

Return on Investment (ROI) is a fundamental metric used to evaluate the profitability of an investment. It measures the gain or loss generated on an investment relative to its initial cost. ROI is typically expressed as a percentage and is calculated as: (Current Value of Investment - Cost of Investment) / Cost of Investment. A positive ROI indicates a profit, while a negative ROI indicates a loss. It’s a simple, widely used metric for comparing the efficiency of different investments.

Annualized Return: Standardizing Performance

While ROI gives a snapshot, annualized return adjusts the return of an investment over a specific period (longer than one year) to a yearly average. This allows for a fair comparison between investments held for different durations. For instance, an investment that returned 20% over two years isn’t as good as one that returned 20% over one year. Annualizing standardizes these returns, making them comparable on a per-year basis and providing a clearer picture of long-term growth.

Dividends: Income from Ownership

Dividends are a portion of a company’s profits paid out to its shareholders. Not all companies pay dividends; growth companies often reinvest profits back into the business, while more mature companies might distribute dividends regularly. Dividends can be a significant source of income for investors, particularly those in retirement, and contribute to the total return of an investment. They are typically paid quarterly and can be reinvested to buy more shares, amplifying the power of compounding.

- Dividend Yield: The annual dividend per share divided by the stock’s current share price, expressed as a percentage. It indicates the return on investment from dividends alone.

Earnings Per Share (EPS): A Company’s Profitability Measure

Earnings Per Share (EPS) is a key financial metric that indicates how much net profit a company makes for each outstanding share of common stock. It’s calculated by dividing a company’s net income (minus preferred dividends) by the number of outstanding common shares. A higher EPS generally indicates a more profitable company, and it is a widely watched indicator for assessing a company’s financial health and potential for growth. Investors often look at EPS trends over time.

Price-to-Earnings (P/E) Ratio: Valuation at a Glance

The Price-to-Earnings (P/E) ratio is one of the most popular valuation metrics for stocks. It measures a company’s current share price relative to its per-share earnings. Calculated as: Market Value Per Share / Earnings Per Share. The P/E ratio indicates how much investors are willing to pay for each dollar of a company’s earnings. A high P/E ratio might suggest that investors expect high future growth, while a low P/E ratio could indicate an undervalued stock or a company with slower growth prospects. It’s best used when comparing companies within the same industry.

Market Capitalization: Company Size

Market capitalization (Market Cap) is the total value of a company’s outstanding shares. It’s calculated by multiplying the company’s current stock price by the total number of its outstanding shares. Market cap is used to categorize companies into different sizes:

- Large-Cap: Typically companies with a market cap of $10 billion or more. These are often established, stable companies.

- Mid-Cap: Companies with a market cap between $2 billion and $10 billion. They often represent growth potential beyond large-caps but with more stability than small-caps.

- Small-Cap: Companies with a market cap between $300 million and $2 billion. These are often younger companies with high growth potential but also higher risk.

Market cap is an important factor in asset allocation and understanding the risk/reward profile of different segments of the stock market.

Risk Management and Strategy: Navigating Uncertainty

Investing inherently involves risk, but smart investors employ strategies to manage and mitigate it. These basic investing terms are fundamental to building a resilient portfolio and achieving long-term goals.

Volatility: The Degree of Price Fluctuation

Volatility refers to the degree of variation of a trading price series over time. In simpler terms, it measures how much an investment’s price fluctuates. A highly volatile asset experiences rapid and significant price swings, while a low-volatility asset has more stable prices. While high volatility can present opportunities for quick gains, it also carries a greater risk of significant losses. Understanding an investment’s volatility helps investors assess its risk profile and potential impact on their portfolio.

Asset Allocation: Spreading Across Asset Classes

Asset allocation is the strategic process of dividing an investment portfolio among different asset categories, such as stocks, bonds, and cash equivalents. The goal is to balance risk and reward by adjusting the percentage of each asset in relation to an investor’s goals, time horizon, and risk tolerance. For instance, younger investors with a longer time horizon might opt for a higher percentage of stocks (more aggressive), while those nearing retirement might prefer a higher percentage of bonds (more conservative). This is a cornerstone of effective portfolio management, and platforms like assetbar often assist users with optimized asset allocation.

Dollar-Cost Averaging: Smoothing Out Market Swings

Dollar-cost averaging (DCA) is an investment strategy in which an investor invests a fixed amount of money at regular intervals (e.g., $100 every month) into a particular asset, regardless of its price. This strategy helps to reduce the impact of volatility because you buy more shares when prices are low and fewer shares when prices are high, ultimately leading to a lower average cost per share over time. DCA is particularly effective for long-term investors and is a common practice in micro-investing and regular contributions to retirement accounts. Discover how dollar-cost averaging can benefit your investment strategy.

Portfolio Rebalancing: Staying on Track

Portfolio rebalancing is the process of adjusting the weightings of assets in a portfolio back to their original target allocations. Over time, the performance of different assets can cause a portfolio’s allocation to drift from its intended targets. For example, if stocks perform exceptionally well, they might grow to represent a larger percentage of your portfolio than initially desired. Rebalancing involves selling some of the outperforming assets and buying more of the underperforming assets to restore the desired proportions. This systematic approach helps maintain the intended risk level and ensures your portfolio remains aligned with your financial goals.

Risk Tolerance: Your Comfort Zone with Loss

Risk tolerance refers to an individual’s willingness and ability to take on financial risk. It’s a critical factor in determining an appropriate investment strategy. Investors with a high risk tolerance might be comfortable with more volatile investments in pursuit of higher returns, understanding that they might experience significant losses. Those with a low risk tolerance prefer safer, less volatile investments, even if it means lower potential returns. Understanding your own risk tolerance is fundamental to building a portfolio that allows you to sleep soundly at night, regardless of market fluctuations.

Understanding Costs and Fees: The Hidden Impact on Returns

Every investment comes with associated costs. While some are obvious, others can be subtle but significantly impact your long-term returns. Being aware of these basic investing terms related to fees is essential for maximizing your net gains.

Expense Ratios: The Cost of Fund Management

For mutual funds and ETFs, the expense ratio is a crucial fee to understand. It’s an annual fee charged as a percentage of your investment to cover the fund’s operating expenses, including management fees, administrative costs, and marketing expenses. For example, an expense ratio of 0.50% means you pay $5 annually for every $1,000 invested. Even small differences in expense ratios can add up to substantial amounts over decades due to the power of compounding. Passively managed index funds and many ETFs typically have much lower expense ratios than actively managed funds.

Commission Fees: Trading Costs

A commission fee is a charge levied by a broker or financial institution for executing a trade (buying or selling securities). Historically, commissions were a significant cost for investors, but with the rise of discount brokers and robo-advisors (like assetbar), many platforms now offer commission-free trading for stocks and ETFs. However, commissions can still apply to certain types of trades, options, or mutual funds, so it’s important to check the fee schedule of your brokerage.

Management Fees: For Professional Oversight

Management fees are charges paid to investment managers or financial advisors for overseeing and managing your investment portfolio. These fees can be part of a fund’s expense ratio or a separate charge for personalized advisory services. They are typically calculated as a percentage of the assets under management (AUM). While professional management can be valuable, it’s crucial to understand the fee structure and ensure the value provided justifies the cost, especially for asset allocation services.

Advisory Fees: For Personalized Guidance

Separate from fund management fees, advisory fees are paid to financial advisors for personalized financial planning, investment advice, and portfolio management services. These fees can be structured in several ways: a percentage of AUM, an hourly rate, a flat fee, or a combination. When working with a financial advisor, understanding their fee structure and how it aligns with your financial goals is paramount. Robo-advisors often offer a lower-cost alternative for basic advisory services.

Investment Accounts and Tax Implications: Navigating the Tax Landscape

The type of account you use to hold your investments can have significant tax implications, affecting your net returns. Understanding these basic investing terms related to accounts and taxes is vital for tax-efficient investing.

Taxable Brokerage Accounts: Flexible but Taxed

A taxable brokerage account is a standard investment account where earnings and capital gains are subject to taxes in the year they are realized. There are no contribution limits, and you can withdraw funds at any time. While offering maximum flexibility, these accounts do not provide the tax advantages of retirement accounts. Interest income, dividends, and capital gains (when you sell an investment for a profit) are typically taxable. Understanding the difference between short-term and long-term capital gains is important here.

Retirement Accounts (401(k), IRA): Tax-Advantaged Growth

Retirement accounts are specially designed investment vehicles that offer significant tax benefits to encourage saving for retirement. The two most common types for retail investors are 401(k)s and Individual Retirement Accounts (IRAs).

- 401(k): An employer-sponsored retirement plan that allows employees to contribute a portion of their salary before taxes are withheld. Contributions and earnings grow tax-deferred until retirement. Many employers also offer a matching contribution, which is essentially “free money.”

- Individual Retirement Account (IRA): A personal retirement savings plan.

- Traditional IRA: Contributions are often tax-deductible in the year they are made, and earnings grow tax-deferred. You pay taxes on withdrawals in retirement.

- Roth IRA: Contributions are made with after-tax dollars, meaning they are not tax-deductible. However, qualified withdrawals in retirement are entirely tax-free.

The choice between a Traditional and Roth account often depends on your current income level and expected tax bracket in retirement. These accounts are cornerstones of long-term wealth building due to their powerful tax advantages. Explore different retirement account options for your future.

Capital Gains: Profits from Selling Investments

Capital gains are the profits realized when you sell an investment for more than its purchase price (its “cost basis”). These gains are subject to taxation. The tax rate applied depends on how long you held the investment:

- Short-Term Capital Gains: Gains from assets held for one year or less are typically taxed at your ordinary income tax rate, which can be higher.

- Long-Term Capital Gains: Gains from assets held for more than one year are taxed at preferential, lower rates. This encourages long-term investing.

Understanding the distinction is crucial for tax planning and can influence your holding periods for various investments.

Tax-Loss Harvesting: Reducing Your Taxable Income

Tax-loss harvesting is a strategy investors use to reduce their tax liability by selling investments at a loss to offset capital gains and, in some cases, a limited amount of ordinary income. For example, if you realize $5,000 in capital gains from one investment, you can sell another investment that has lost $5,000 to offset those gains, effectively reducing your taxable gains to zero. You can also use up to $3,000 of net capital losses to offset ordinary income each year, carrying forward any excess losses to future years. This strategy needs careful planning to avoid wash-sale rules.

The Role of Financial Professionals and Resources: Getting Help and Staying Informed

You don’t have to navigate the investment world alone. Various professionals and resources are available to assist you. Understanding these basic investing terms will help you choose the right support for your financial journey.

Financial Advisors: Personalized Guidance

A financial advisor is a professional who helps individuals and organizations manage their money. They can provide a wide range of services, including investment advice, retirement planning, estate planning, and insurance analysis. Advisors can be fee-only (paid directly by clients), commission-based (paid by selling products), or fee-based (a combination). When choosing an advisor, it’s important to look for a fiduciary, meaning they are legally obligated to act in your best interest.

Robo-Advisors: Automated, Low-Cost Advice

A robo-advisor is a digital platform that provides automated, algorithm-driven financial planning services with little to no human supervision. These platforms typically offer automated portfolio management, rebalancing, and tax-loss harvesting based on your risk tolerance and financial goals, often at a much lower cost than traditional human advisors. assetbar’s micro-investing platform utilizes robo-advisory features to simplify asset allocation and make sophisticated investing accessible to retail investors, even with small amounts of money.

Financial News and Research: Staying Informed

Staying updated with financial news and research is crucial for making informed investment decisions. This includes reading reputable financial publications, analyzing company reports (like annual reports and quarterly earnings statements), following economic indicators, and understanding market trends. While it’s important not to react to every piece of news, being informed helps you understand the broader economic landscape and the factors influencing your investments.

Micro-Investing Platforms (like assetbar): Investing Made Accessible

Micro-investing platforms (like assetbar) are financial services that allow individuals to invest very small amounts of money, often by rounding up everyday purchases or setting up recurring small contributions. These platforms break down the traditional barriers to entry for investing, making it accessible to a broader audience, including those with limited capital. They often simplify the investment process, provide diversified portfolios, and encourage consistent investing through dollar-cost averaging, making them an excellent starting point for new investors.

Investment Vehicle Comparison Table

To help illustrate the differences among common investment vehicles, here’s a comparative overview:

| Investment Vehicle | Primary Goal | Typical Risk Level | Income Potential | Liquidity | Key Benefit for Retail Investors |

|---|---|---|---|---|---|

| Stocks (Equities) | Capital Appreciation | Medium to High | Dividends, Capital Gains | High | High growth potential; direct ownership in companies. |

| Bonds (Fixed Income) | Income Generation, Capital Preservation | Low to Medium | Interest Payments (Coupon) | Medium to High | Stability, predictable income, portfolio diversification. |

| Mutual Funds | Diversification, Professional Management | Varies (Fund Specific) | Dividends, Interest, Capital Gains | High (daily NAV pricing) | Instant diversification, managed by experts. |

| Exchange-Traded Funds (ETFs) | Diversification, Index Tracking | Varies (Fund Specific) | Dividends, Capital Gains | High (trades like stocks) | Low cost, diversification, trading flexibility. |

| Real Estate (REITs) | Income Generation, Long-term Growth | Medium | High Dividends | Medium (traded on exchanges) | Exposure to real estate without direct property ownership; high dividends. |

Conclusion: Your Path to Financial Empowerment

Mastering these basic investing terms is more than just memorizing definitions; it’s about building a foundational understanding that empowers you to take control of your financial future. From the fundamental difference between saving and investing to the nuances of asset allocation and tax-efficient strategies, each term unlocks a new level of insight into how markets work and how you can participate effectively.

At assetbar, our mission is to make financial literacy and successful investing accessible to everyone. By demystifying the jargon and providing clear explanations, we aim to equip retail investors like you with the knowledge and tools needed to make smart, confident investment decisions. Remember, investing is a journey of continuous learning. Start small, stay consistent, diversify your portfolio, and always seek to expand your understanding. With a solid grasp of these basic investing terms, you are well on your way to achieving your wealth-building goals and securing a prosperous future.

Frequently Asked Questions

Q1: What are the absolute must-know basic investing terms for a beginner?

A1: For a beginner, the most crucial basic investing terms to understand include “investment,” “savings,” “compounding,” “diversification,” “risk and return,” “stocks,” “bonds,” “ETFs,” and “mutual funds.” Grasping these foundational concepts will provide a solid framework for making your first investment decisions and understanding broader market dynamics.

Q2: How do I know if I have a high or low risk tolerance?

A2: Your risk tolerance is your willingness and ability to endure potential losses for higher gains. You can assess it by considering your financial goals (time horizon), current financial situation (emergency fund, debt), and emotional reaction to market fluctuations. If the thought of losing a significant portion of your capital keeps you up at night, you likely have a lower risk tolerance. Many brokerage platforms, including assetbar, offer questionnaires to help you determine your risk tolerance more accurately.

Q3: What’s the main difference between a mutual fund and an ETF?

A3: Both mutual funds and ETFs pool money from investors to buy a diversified portfolio of securities. The main difference lies in how they are traded and priced. Mutual funds are priced once a day after the market closes (based on their Net Asset Value or NAV) and are bought/sold directly from the fund company. ETFs, on the other hand, trade like individual stocks on exchanges throughout the day, allowing for real-time buying and selling at fluctuating market prices. ETFs often have lower expense ratios and more trading flexibility.

Q4: Why is diversification so important, and how can I achieve it with basic investing terms?

A4: Diversification is crucial because it helps reduce risk by spreading your investments across various assets, industries, and geographies. If one investment performs poorly, others may perform well, cushioning the impact on your overall portfolio. You can achieve diversification by investing in a mix of stocks and bonds, using broad-market ETFs or mutual funds that hold hundreds or thousands of different securities, and considering different asset classes like real estate (via REITs) or commodities.

Q5: Are all investment accounts taxable?

A5: Not all investment accounts are fully taxable in the same way. While standard brokerage accounts (taxable accounts) generate taxable events from interest, dividends, and capital gains in the year they occur, retirement accounts like 401(k)s and IRAs (Traditional and Roth) offer significant tax advantages. Traditional accounts allow tax-deferred growth (you pay taxes upon withdrawal in retirement), while Roth accounts offer tax-free withdrawals in retirement (after-tax contributions). Understanding these differences is key to optimizing your tax strategy.